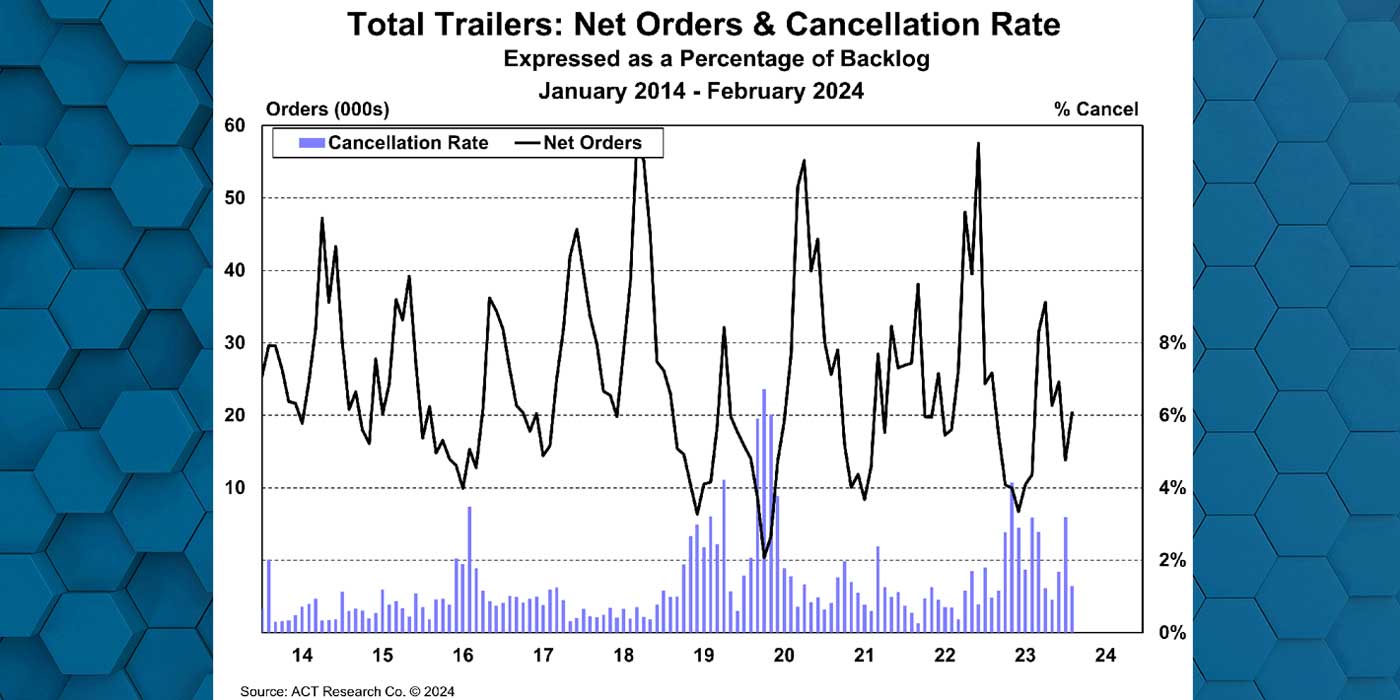

Preliminary NA Class 8 net orders in September were 53,700 units, while NA Classes 5-7 net orders were 26,600 units. Complete industry data for September, including final order numbers, will be published by ACT Research in mid-October.

“The strength in orders reflects OEMs’ having fully opened their orderboards for 2023 a bit earlier than normal, as the seasonally weak period for truck orders typically runs May-September,” said Eric Crawford, vice president and senior analyst, ACT. “As such, typical seasonal adjustment is not as useful a statistic this month: September’s orders translate to 60,900 on an SA basis (+161% m/m, +94% y/y), equivalent to more than 730k units on a seasonally adjusted annualized basis.”

ACT’s State of the Industry: Classes 5-8 Vehicles report provides a monthly look at the current production, sales, and general state of the on-road heavy and medium duty commercial vehicle markets in North America. Additionally, Class 5 and Classes 6-7 are segmented by trucks, buses, RVs, and step van configurations.

“Using an October seasonal adjustment factor (typically the beginning of next-year orders) would translate to 43,800 units, equivalent to ~526k on an annualized basis. September Class 8 orders were sensational no matter how you slice the data,” Crawford said. “Over the past 12 months, 249,800 Class 8 orders have been booked.” About medium-duty orders, he added, “MD demand was strong. September Classes 5-7 orders increased 39% sequentially (+7% y/y) to 26,600 units.”

The Class 8 market is segmented into trucks and tractors, with and without sleeper cabs. The report includes a six-month industry build plan, a backlog timing analysis, historical data from 1996 to the present in spreadsheet format, and a ready-to-use graph package. A first-look at preliminary net orders is also published in conjunction with this report.