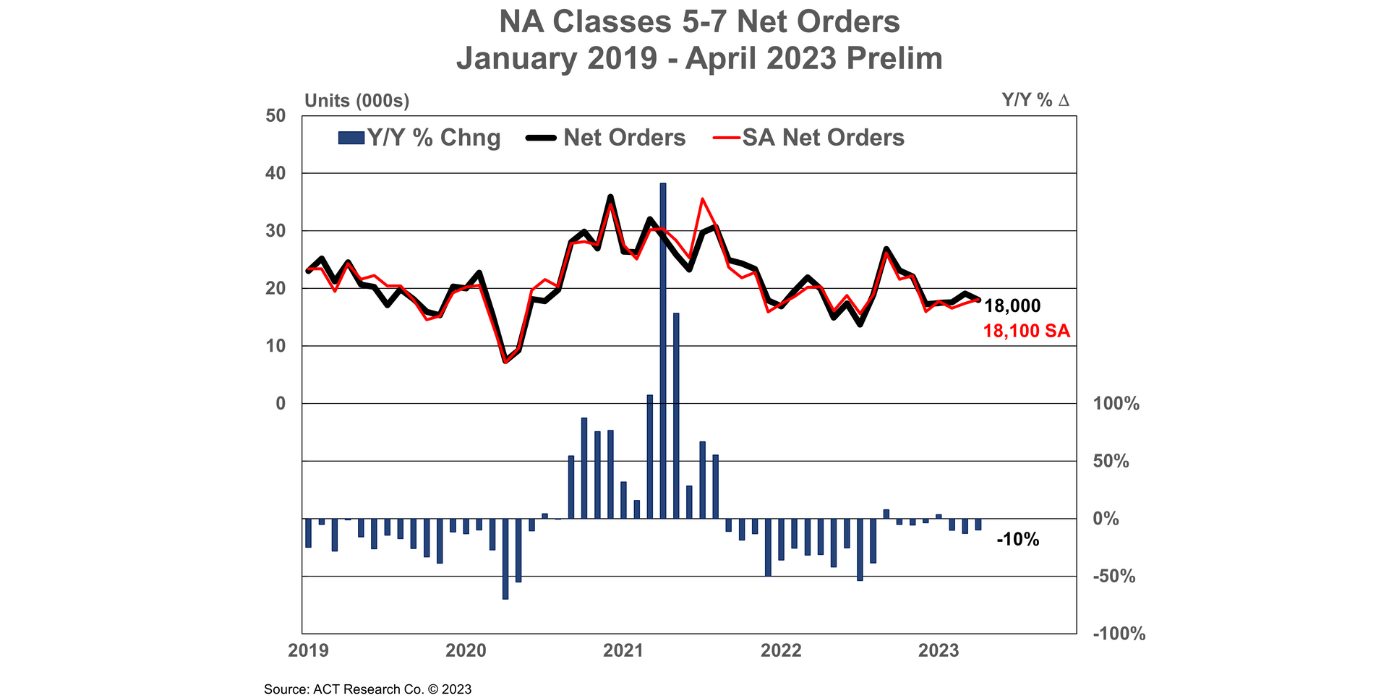

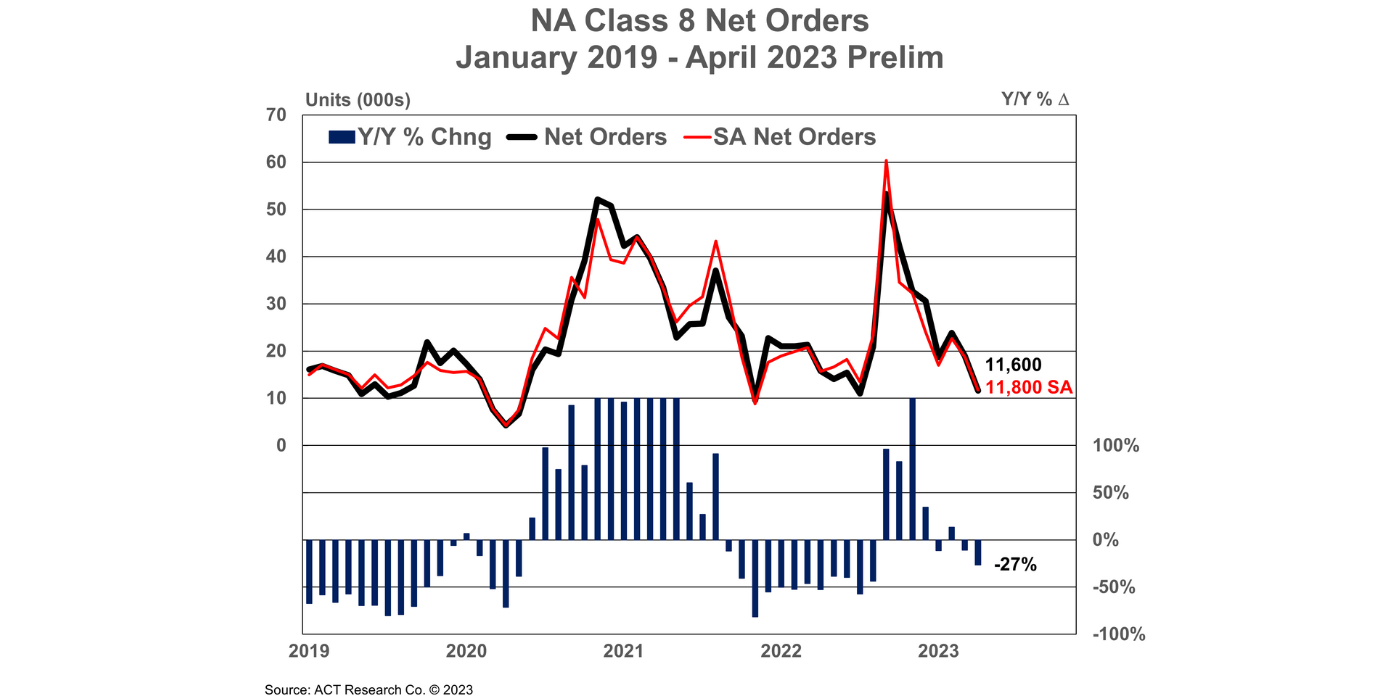

Research found from ACT Research found that North American Class 8 net orders in April were at 11,600 units, down 27% year-over-year (-39% month-over-month), while preliminary Classes 5-7 net orders were at 18,000 units, down 10% y/y (-6% m/m).

“Given robust Class 8 orders into year end, ensuing backlog support, and normal seasonal order patterns, orders were expected to moderate into Q2; we expected [standalone] orders in a range of 15-20k units per month into mid-Q3 of 2023. Coupling those items with increasingly cautious readings from the ACT Class 8 Dashboard, April orders were weaker than expected on a standalone basis but bring the YTD monthly [standalone] average to 17,500, squarely in line with our view,” shared Eric Crawford, vice president and senior analyst at ACT Research.

“The recent turmoil in the banking sector likely tightened credit conditions for some industry participants and may have played a factor in exacerbating April’s weakness,” he added. “Thus, while we expect orders to remain at subdued levels into mid-Q3, we are not inclined to think April’s order activity represents the likely run rate going forward.”

Additionally, Crawford highlighted that medium-duty demand only declined y/y by single digits, a change of pace compared to the previous two months. He stated that April Classes 5-7 orders declined 10% y/y (-6% m/m) to 18,000 units.