ACT Research recently hosted their industry update concerning the state of economics, transportation and commercial vehicles. The abundance of forecasts, statistics and charts can feel like information overload, so let us give you the run-down.

Presented by Kenny Veith, president and senior analyst; Eric Crawford, vice president and senior analyst; Steve Tam, vice president and analyst; and Jennifer McNealy, director, CV Market and Publications; the research team focused on the different aspects of the industry currently impacted by economics.

The presentation was kicked off with some good news and some bad news concerning some diametrically opposed forces equally impacting the industry:

Bad News

• Interest rates are up and more hikes are expected due to inflation;

• Yield curve(s) inverted ;

• Consumer goods spending binge is over;

• Sharp roll-off in trucking spot rates;

• Global economies wobble; and

• Supply chain restraints persist.

Good News

• North American economic demand hanging on;

• Low unemployment and strong job market; and

• Strong consumer and business balance sheets.

What’s the impact on the freight environment?

The Russia-Ukraine conflict continues to exacerbate the economic issues of the post-pandemic period causing a corrosive effect of inflation on consumer consumption. Freight recession is certain. Inflation continues to trim trucking volumes flat to down which should help ease the supply chain pressure.

“It’s not shocking that after two years of a spending surge that we start to see goods spending come down. The downturn in goods spending is related to the corrosive impact of higher prices and lower incomes,” Veith said.

Along with the freight demand also comes a demand for drivers. With driver schools full and BLS employment strong, this trend is expected to continue.

Understanding where the market has been so we know where it’s going

Q1 ‘20

- Truck orders canceled/pulled forward

- Market attempts to bring balance

- Prices bottom out

Q2 ‘20

- Loose to balanced capacity

- Prices rise

- No/little incremental equipment growth

Q4 ‘21

- Carrier margins were up

- New trucks purchased

- Driver wages up

- Capacity grows

Q1 ‘22

- Use and investment in private fleet

- Demand down and/or supply up

- Prices start sliding

“Used truck prices are going through the roof because of the 11% growth of freight in 2021 and OEM inability to produce vehicles to keep up with demand,” Veith said.

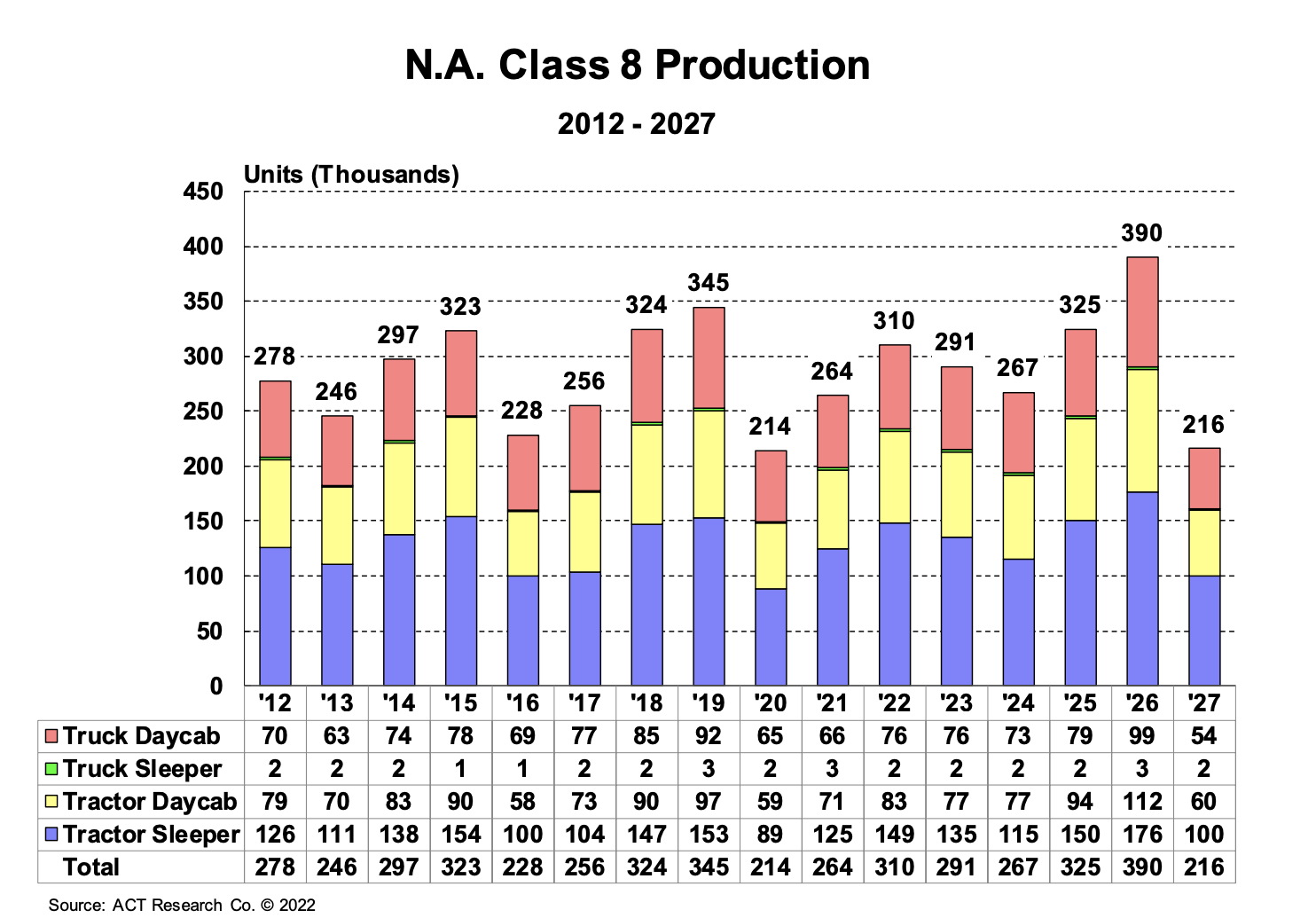

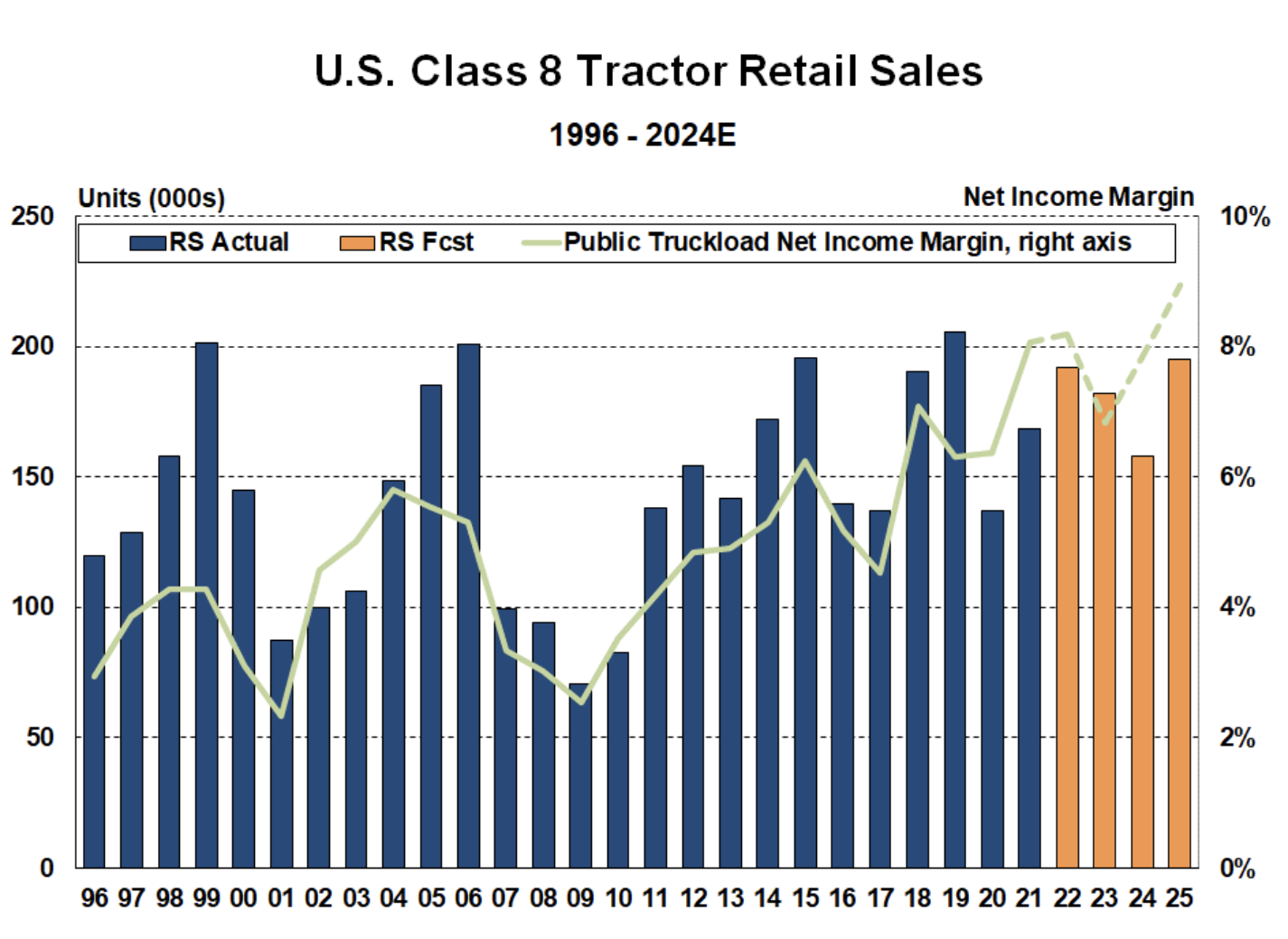

Where are we in the cycle?

Here’s a handy chart with historic data and a truck production forecast:

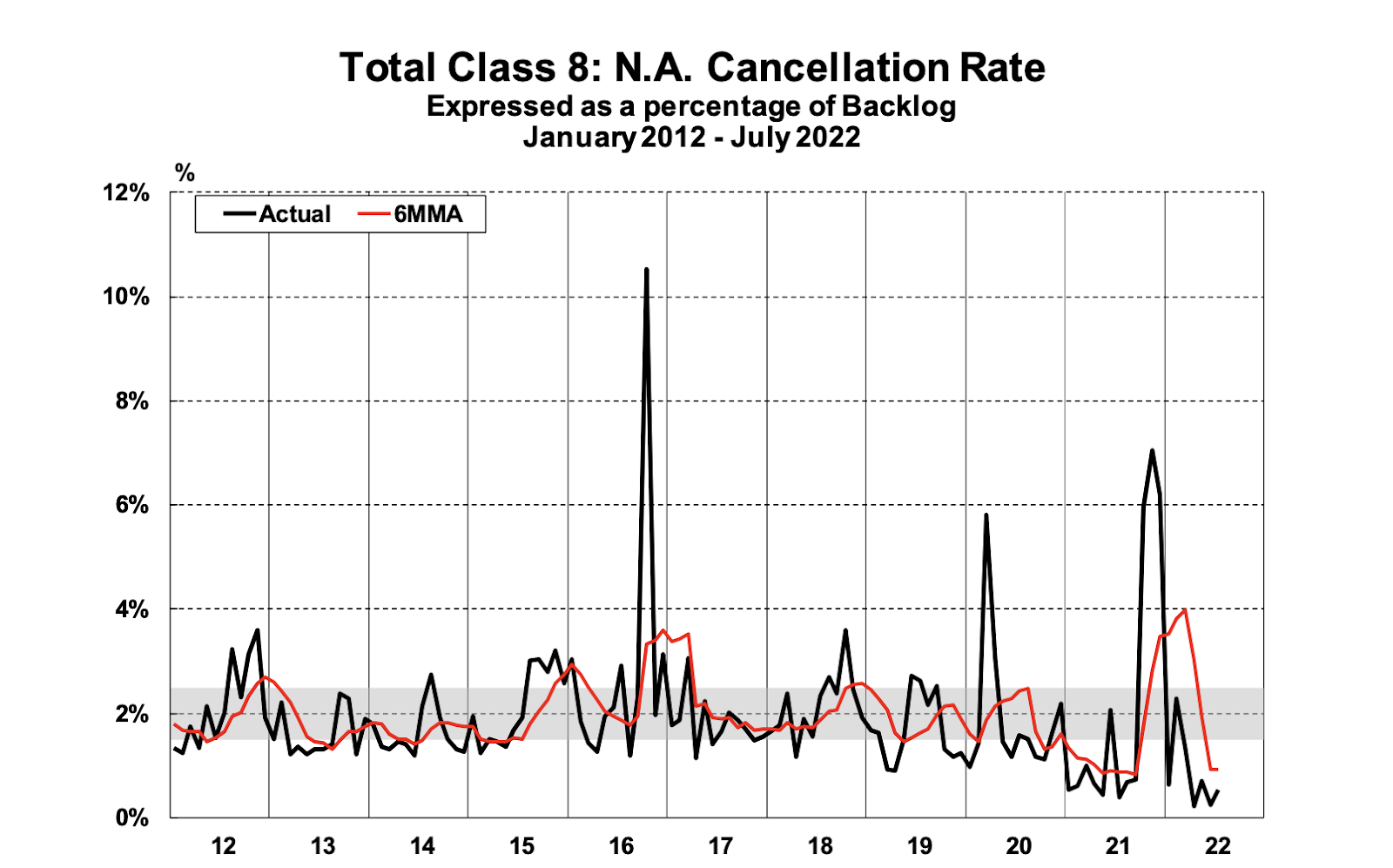

Cancellations: Miniscule by historical standards, ACT Research noted. Customers do not have enough equipment and are adamantly maintaining orders–a sentiment that was confirmed by Mack Trucks during its own market update. [LINK: https://www.fleetequipmentmag.com/mack-trucks-recession-demand/]

What does this all mean going forward?

For next year, the ACT Research team said to expect pent-up demand early on and late pre-buying, with prebuy in approximately 10% of the market ahead of CARB’s 2024 Clean Truck Initiative. Additionally, tailwinds from infrastructure should ease manufacturing decline, the company noted.

Looking beyond to 2024, ACT Research forecasted another approximate 10% of market pre-buying as states follow CARB mandates, an economic rebound gets started and spot-rate recovery begins in earnest, planting seeds for CV demand cycle

Profitability by the truckload

These conditions provide the industry with the best-ever financial situation, ACT Research noted. Risk of a larger downturn mitigated by higher industry cost base and public fleet performance likely much better than average fleet.

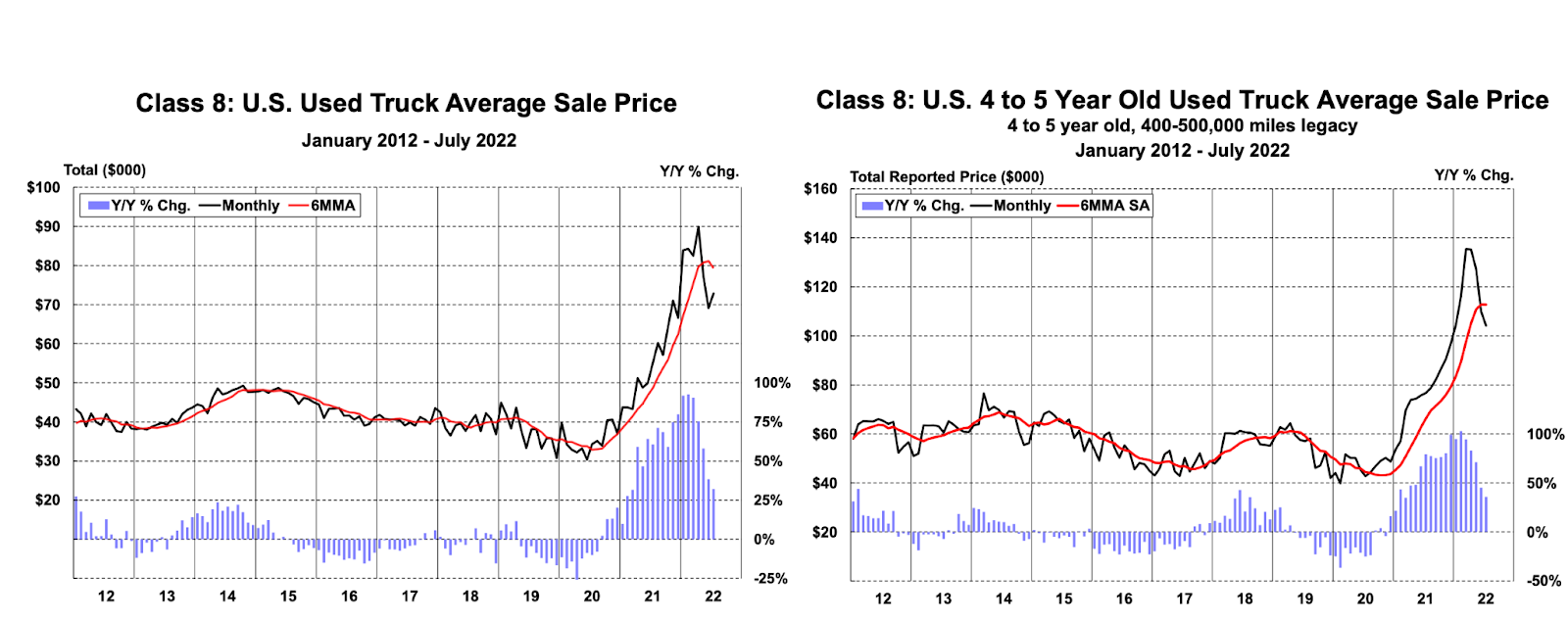

Class 8 truck sales update

The average retail cost in July was $91,900. To put it into perspective, that is -1% month over month, +43% year over year and +69% year to date. Due to slower freight markets and lack of inventory, demand continues to lag. Miles and age additionally continue to increase subtly.

“We’re also challenged, of course, on the supply side. There are comments regarding production and not being able to make as many new vehicles as customers are demanding has slowed the flow of trades in the secondary market and has limited the supply of used equipment.” Crawford said.

Prices are on the backside of the wave

The export market

As of now, there are simply not enough domestic trucks, this, however, is not just a supply chain issue as it is happening internationally. In turn, the industry is seeing demand for the export market fall off.

Medium-duty truck market

When it comes to the medium-duty market, customers are beginning to see some progress:

- Backlog rolled-over, but still 3x average

- BL/BU coming down, but still high

IN/RS ratio going the wrong direction:

- Sales trending lower, inventory drifting higher

Market forecast has tipped further into decline:

- 2022: Build (-2%) and retail sales (-6%)

- Reversal of fortunes sets expectations for 2023 growth

Service-cetric economic growth supporting medium-duty truck demand

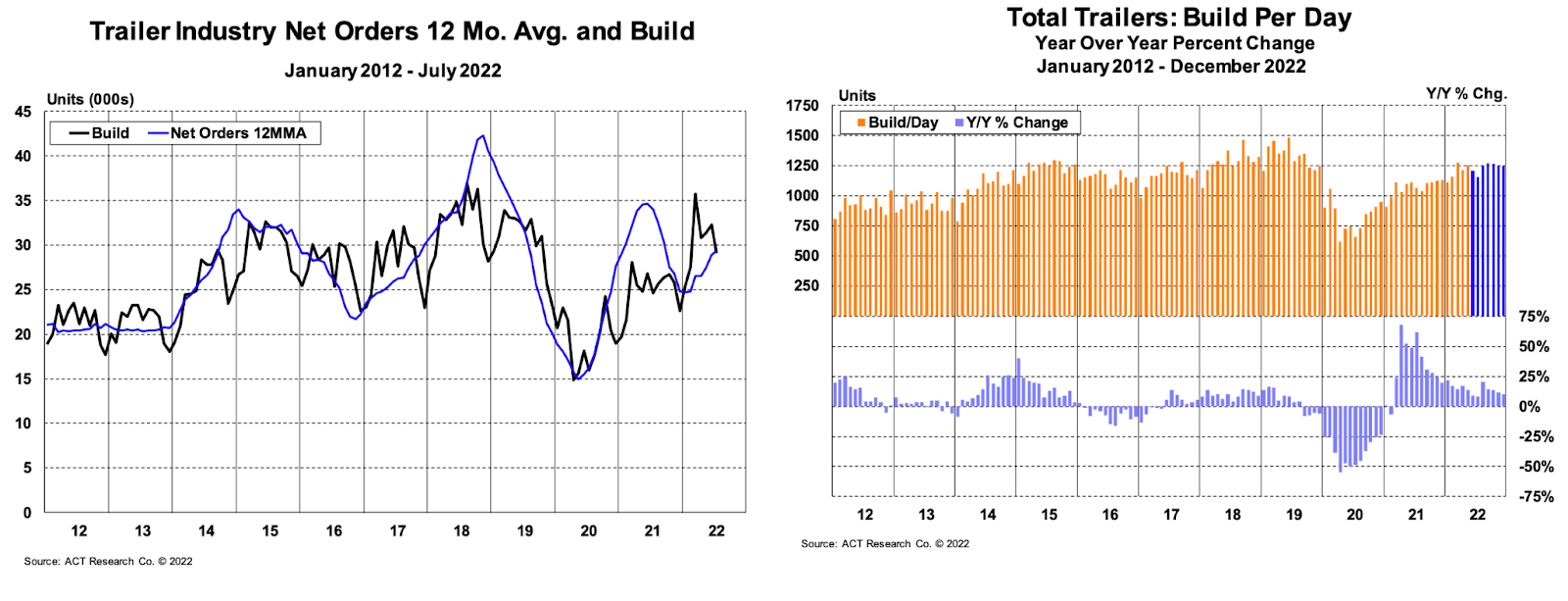

Trailer market overview

Strong demand continues in the trailer market and supply constraints begin to ease. Next year order boards are already full with seasonal backlogs well into 2023. Orders continue to be weak and cancellations are moderate. Backlogs are down, however, they originally started from a high level. While historically low in July, build is gaining traction and an uptick is expected through the end of the year depending on the state of the supply chain.