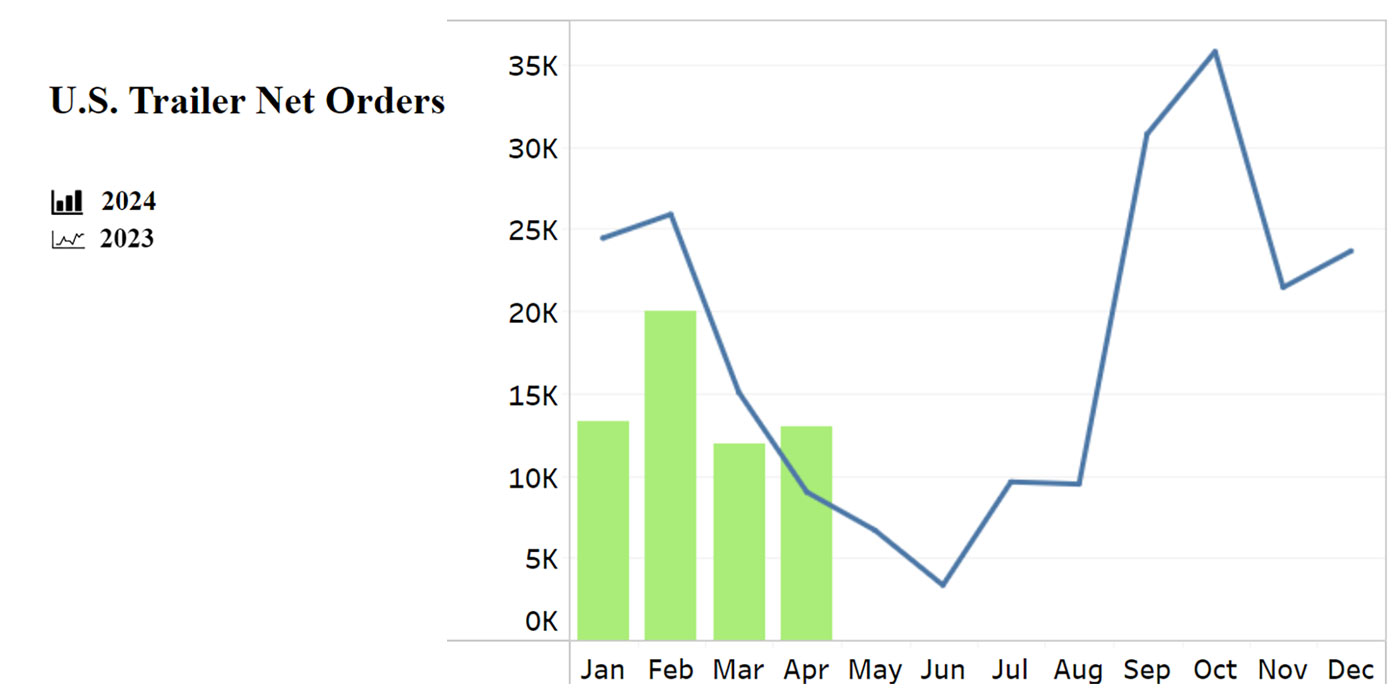

March trailer net orders, at 13,600 units, were nearly 25% lower year-over-year, and 7,000 units below February’s intake, according to ACT Research. ACT notes that this brings Q1 2024 net orders to 48.3k units, down 29% from Q1 2023’s faster paced order environment, with its pent-up demand and moderately congested supply chain.

“Seasonally adjusted, March’s orders were 13,800 units compared to a 20,200 seasonally adjusted rate in February,” said Jennifer McNealy, director of research analysis and publications at ACT Research. “On that basis, orders decreased 32% m/m. Dry van orders contracted 28% y/y, with reefers up 6%, and flats 40% lower compared to March 2023.”

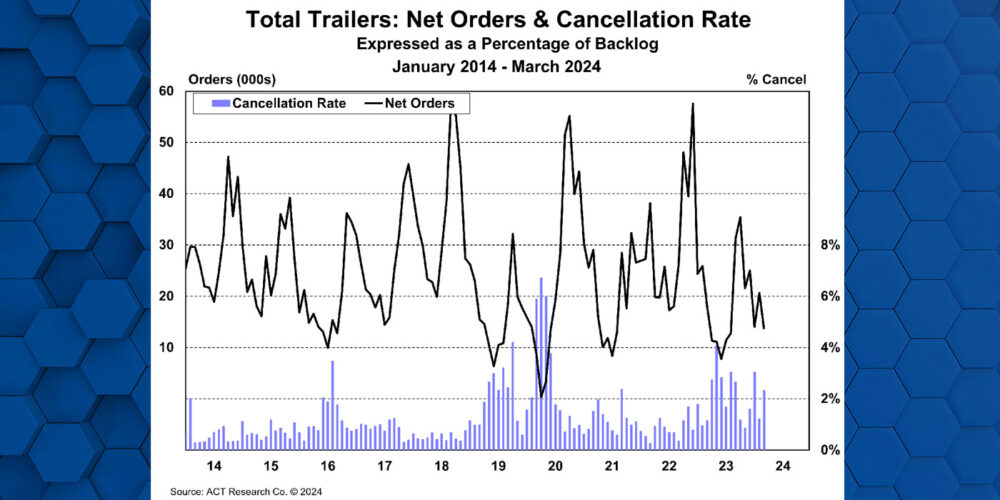

“Total cancellations oscillated to the higher side of the pendulum in March,” McNealy added. “Thanks to a smaller denominator, the cancellation rate jumped to 2.3% of the backlog, from February’s improved 1.3% rate. Seven of ten markets tracked remained above the 1% mark, with OEMs indicating cancellations from fleets and dealers.”

McNealy concluded, “Capex remains constrained, and this means fleets are forced to make even more difficult decisions about how to spend their money. In the current carrier profit trough, the decision is compounded by the impending EPA regulations for power units, which are expected to have materially higher costs. Softer fleet demand isn’t the only thing weighing on the minds of trailer manufacturers, though, as elevated dealer inventories have resulted in waning demand there, too.”