According to ACT Research’s (ACT) latest State of the Industry: NA Classes 5-8 Report, surging inflation, the Fed hiking interest rates into a potential recession, and supply-chain disruptions remain overarching themes.

“The prospect of a US recession has grown materially since Russia’s invasion of Ukraine, and as of the July issue of ACT’s NA OUTLOOK report, a 2023 recession is now the base-case expectation, with freight volumes beginning to contract in Q3’22,” according to Kenny Vieth, president and senior analyst, ACT Research. “Meanwhile, supply-chain disruptions remain a wild card, as the war in Ukraine continues and China announced fresh lockdowns following another surge in COVID infections.”

When asked about inflation, Vieth explained, “The takeaway for us is that interest rate hikes to date have not yet slowed inflation sufficiently, meaning the Fed is likely to remain aggressive, risking a deeper recession in 2023 as they work to rein in inflation.” Regarding supply-chain concerns and impacts to commercial vehicle markets, he commented, “The prevailing theme cycle-to-date has been one of whack-a-mole, i.e. as shortages of one component are alleviated, another issue arises. Russia and China issues aside, the past two months have seen modest OEM beats of their medium-duty and heavy-duty build plans, suggesting that availability, and possibly visibility, is improving.”

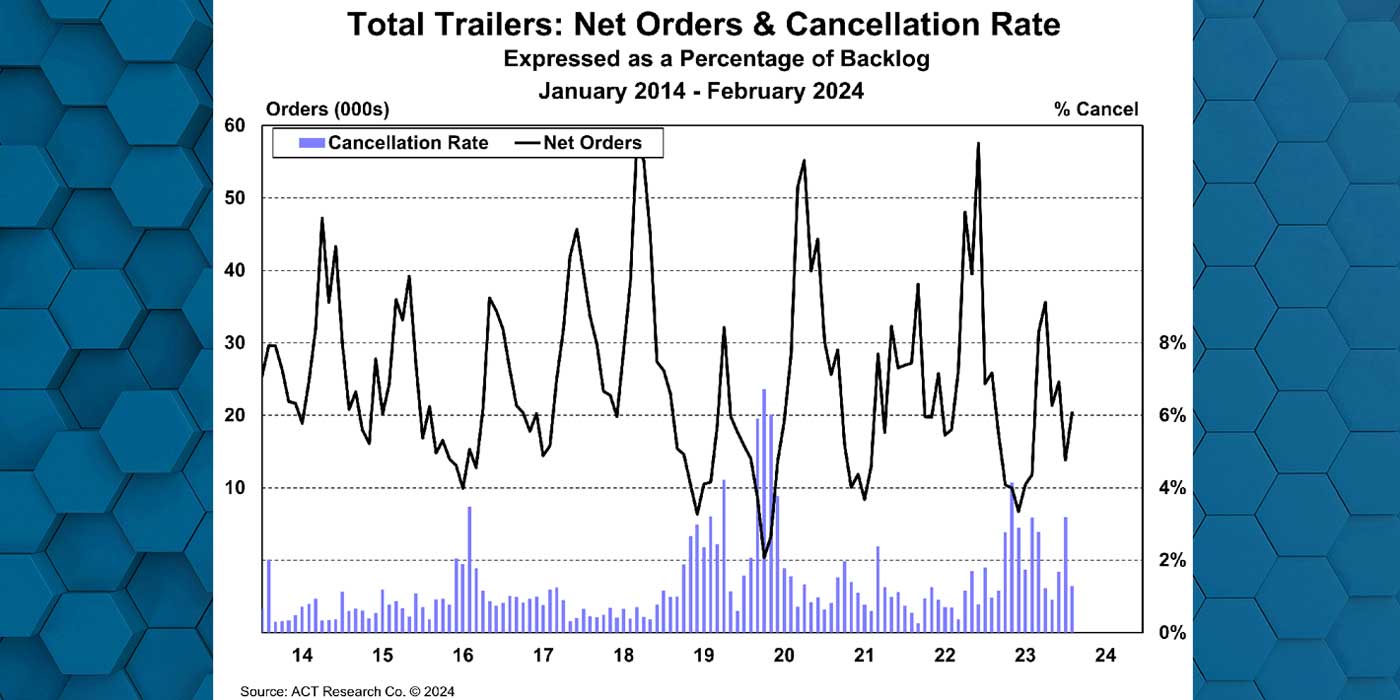

ACT’s State of the Industry: NA Classes 5-8 report provides a monthly look at the current production, sales, and general state of the on-road heavy and medium duty commercial vehicle markets in North America. It differentiates market indicators by Class 5, Classes 6-7 chassis and Class 8 trucks and tractors, detailing measures such as backlog, build, inventory, new orders, cancellations, net orders, and retail sales.

Additionally, Class 5 and Classes 6-7 are segmented by trucks, buses, RVs, and step van configurations, while Class 8 is segmented by trucks and tractors with and without sleeper cabs. This report includes a six-month industry build plan, backlog timing analysis, historical data from 1996 to the present in spreadsheet format, and a ready-to-use graph package. A first-look at preliminary net orders is also published in conjunction with this report.

“Forward-looking data were largely aligned with expectations in June, while concurrent and trailing indicators were modestly above expectations, as North America’s commercial vehicle markets continue to embody a balancing act between demand-driven potential and supply-side realism,” Vieth said. “For context, we saw Class 8 orders rise 16% sequentially in June, cancellations fall to a 12-year low, build rise to its highest level this cycle, and heavy-duty retail sales jump to their best result of the year.”