According to ACT Research’s (ACT) latest State of the Industry: NA Classes 5-8 Report, Russia/China supply-chain disruptions, raging inflation, higher interest rates, and recession potential continue to dominate the narrative.

“Russian commodities remain locked out of Western markets, Ukraine remains besieged, and China continues to struggle with COVID and lockdowns,” Eric Crawford, vice president and senior analyst, ACT Research. “The battle against inflation is global. U.S. inflation continues to accelerate, prompting the Fed to lift the Fed Funds rate 75 basis points this week, the largest increase since 1994, and markets and economists are increasingly predicting a US recession in 2023.”

When asked what this all means for commercial vehicle markets, Crawford explained, “While Classes 5-8 production exceeded lowered expectations in May and build plans were largely unchanged, supply-chain risks remain elevated. Moreover, we believe the likelihood of a US economic recession is growing and probability of a mild recession is now about as likely as that of our base-case scenario.”

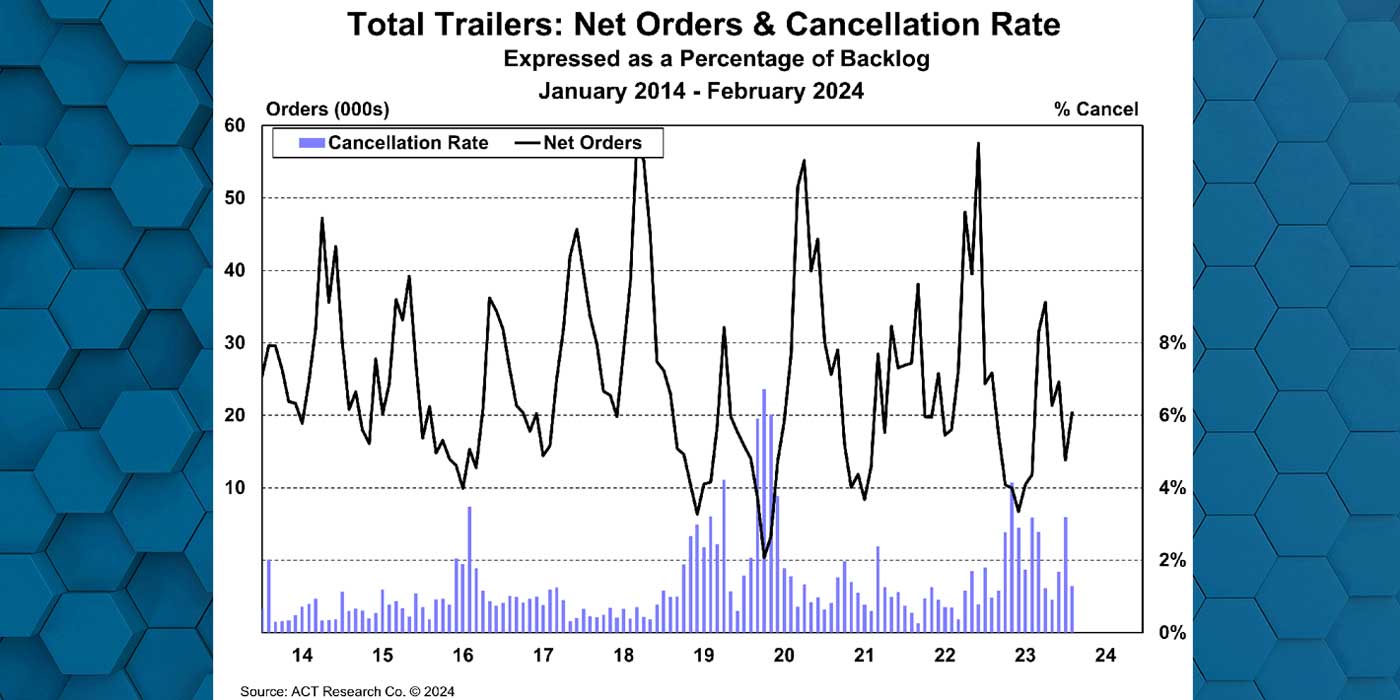

Regarding commercial vehicle segment production and orders, Crawford commented, “Backlogs remain long and order volumes remain constrained. Until build rates find additional traction, orders will largely mirror production levels, but the steep decline in truckload spot rates ex-fuel in recent months will soon impact vehicle demand.”

ACT’s State of the Industry: NA Classes 5-8 report provides a monthly look at the current production, sales, and general state of the on-road heavy and medium duty commercial vehicle markets in North America. It differentiates market indicators by Class 5, Classes 6-7 chassis and Class 8 trucks and tractors, detailing measures such as backlog, build, inventory, new orders, cancellations, net orders, and retail sales. Additionally, Class 5 and Classes 6-7 are segmented by trucks, buses, RVs, and step van configurations, while Class 8 is segmented by trucks and tractors with and without sleeper cabs. This report includes a six-month industry build plan, backlog timing analysis, historical data from 1996 to the present in spreadsheet format, and a ready-to-use graph package. A first-look at preliminary net orders is also published in conjunction with this report.