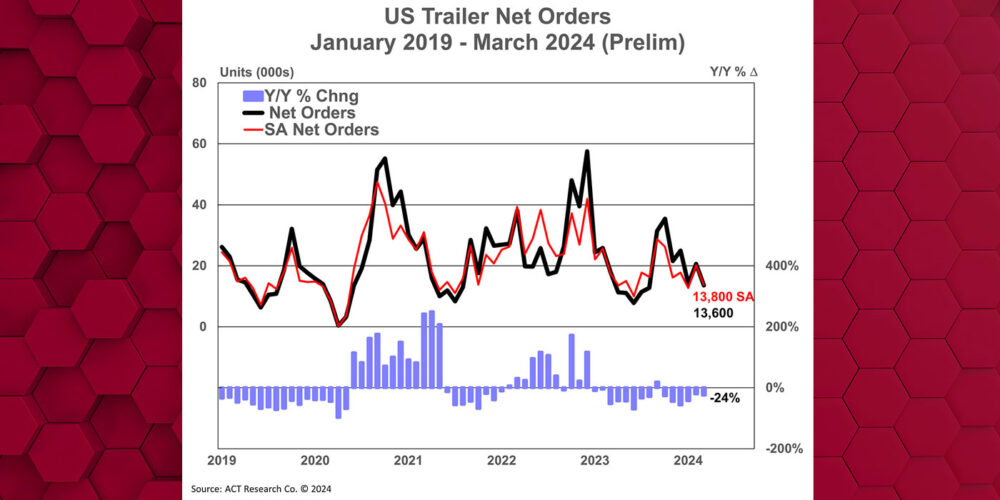

Preliminary NA Class 8 net orders in October were 42,500 units, while NA Classes 5-7 net orders were 23,400 units. Complete industry data for October, including final order numbers, will be published by ACT Research in mid-November.

“The strength in orders reflects, one, OEMs having opened their orderboards for 2023 more broadly, and, two, ongoing pent-up demand, with tailwinds from strong carrier profitability and elevated fleet age proving resilient,” said Eric Crawford, vice president and senior analyst, ACT. “We continue to expect a freight recession, and an eventual economic recession (mild to medium in magnitude), but OEMs at this point have clear visibility to a strong 1H’23 (barring any unforeseen cataclysmic events).

“MD demand was solid, albeit against somewhat challenging comps. Over the past 12 months, the MD market has seen 234,200 orders booked,” he added.

ACT’s State of the Industry: Classes 5-8 Vehicles report provides a monthly look at the current production, sales, and general state of the on-road heavy and medium duty commercial vehicle markets in North America. It differentiates market indicators by Class 5, Classes 6-7 chassis and Class 8 trucks and tractors, detailing activity-related measures such as backlog, build, inventory, new orders, cancellations, net orders, and retail sales. Additionally, Class 5 and Classes 6-7 are segmented by trucks, buses, RVs, and step van configurations. The Class 8 market is segmented into trucks and tractors, with and without sleeper cabs. The report includes a six-month industry build plan, a backlog timing analysis, historical data from 1996 to the present in spreadsheet format, and a ready-to-use graph package. A first-look at preliminary net orders is also published in conjunction with this report.