According to the latest reporting from ACT Research, the rebalancing process in the U.S. freight market is being drawn out by reluctance to part with workers and significant private fleet capacity expansion, even as pressure on fleets worsened this month as diesel prices spiked.

“Although seasonality remains loose and demand soft, spot market dynamics have begun to shift since the end of operations at Yellow on July 31. While this is a game-changer for LTL rates, so far, the truckload market is still loose enough for rates to be largely unaffected. We see the impact growing over time, along seasonal patterns,” shared Tim Denoyer, vice president and senior analyst at ACT Research.

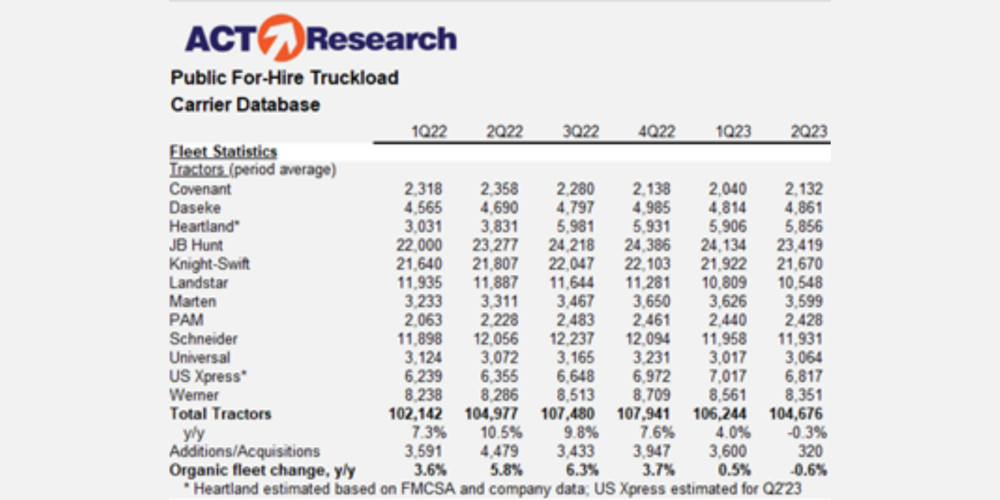

According to ACT, the publicly traded for-hire fleets reduced their collective tractor count by 3% in 1H’23, but Class 8 tractor sales and production are still near maximum levels, adding considerably to the Class 8 tractor fleet. Private fleets are still growing and pulling freight from the for-hire market.

“Class 8 orderswill be very interesting over the next several months and, in our view, pivotal to setting the market tone for 2024,” Denoyer concluded.