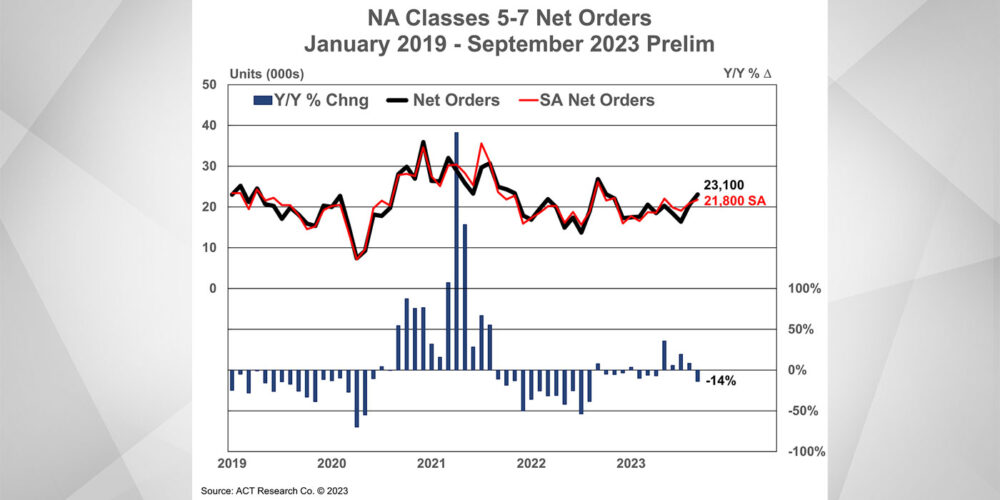

ACT Research reports that September preliminary North American Class 8 net orders came in at 36,800 units, up 67% month-over-month, reflecting the strongest order month in the past year. Classes 5-7 net orders were more trend-like, rising 13% m/m to 23,100 units, according to ACT.

“Between reports of falling carrier income and margins, still sloshy load-to-truck ratios, weak spot rates reported by DAT, and a sense over the past six weeks or so that the U.S. economy’s year-to-date outperformance was starting to lose some momentum, we were unsure how the market would respond when the 2024 orderboards officially opened,” shared Kenny Vieth, president and senior analyst at ACT Research. “One thing we did know was that nearly all the August-ending Class 8 backlog was scheduled for build in 2023, so strong orders are imperative for the industry to maintain current strong production rates very far into 2024.

“While it is too early to infer much from September orders, data from the OEMs confirm the ‘season’ started on the right foot,” he added.