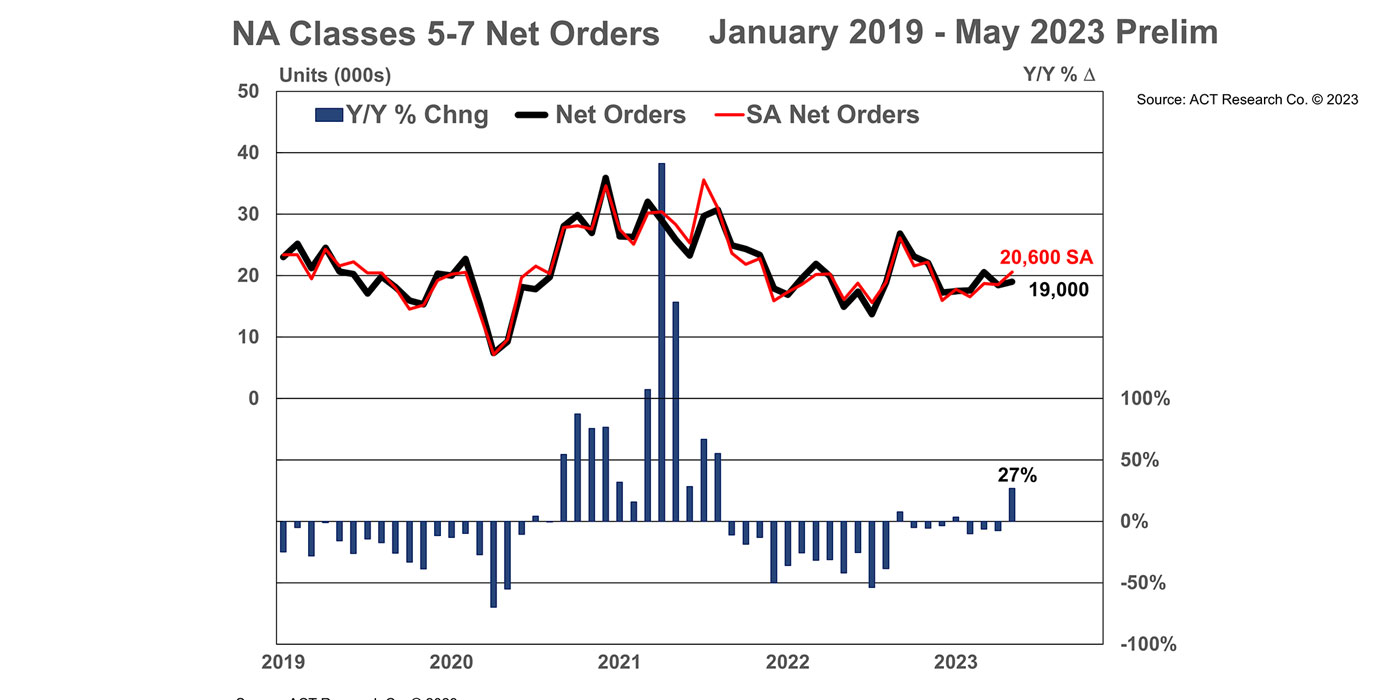

Preliminary NA Class 8 net orders bounced back in May with 15,500 units, up 10% year-over-year (+29% month-over-month), while preliminary Classes 5-7 surged 27% y/y with 19,000 units (+3% m/m), according to ACT Research.

“Given robust Class 8 orders into year end and the ensuing backlog support, coupled with normal seasonal order patterns, orders were expected to moderate into Q2 and remain at relatively soft levels into mid-Q3 of 2023. May orders were in line with this view,” shared Eric Crawford, vice president and senior analyst at ACT Research. “The relatively few build slots still free in [the second half of 2023] suggest order intake is unlikely to find meaningful traction in the coming months.”

Medium-duty demand surged 27% higher y/y to 19,000 units (+3% m/m), reversing course after three straight months of y/y declines, he noted. The seasonally adjusted May intake, at 20,600 units, increased 28% y/y (+11% m/m).