While clouds on the trailer-market horizon bear watching, industry stakeholders remain cautiously optimistic about 2024, according to this month’s issue of ACT Research’s State of the Industry: U.S. Trailers report.

“In addition to an improved longer-term outlook, nearer-term, general business conditions and material supply chains remain on par with July levels in the face of continued strong trailer output,” said Jennifer McNealy, director of CV market research and publications at ACT Research.

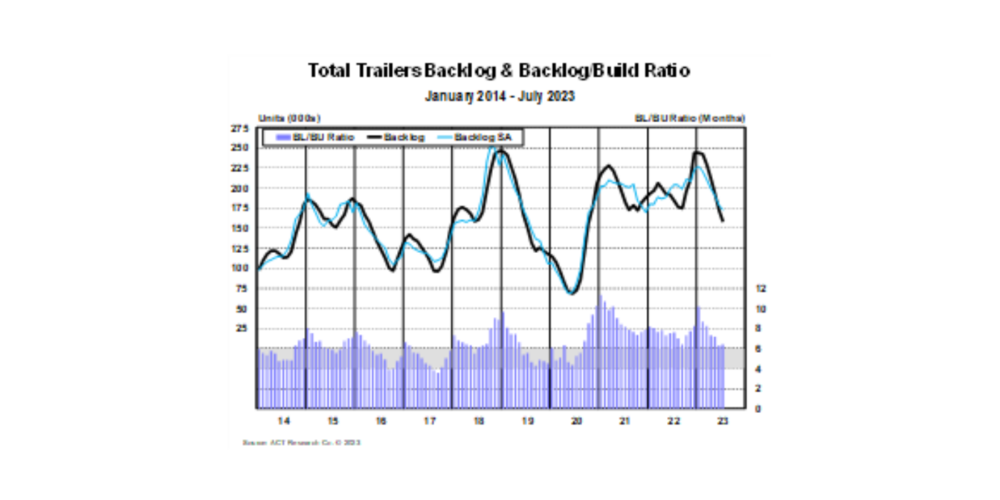

“Supply-chain issues have essentially normalized, and OEMs continue to report smaller, more manageable and less impactful disruptions,” she explained. “Build was 14% lower month-over-month, partly attributable to one less build day in July. As expected, production outpaced orders into July’s annual order trough, dropping trailer backlogs 15% year-over-year. Because large backlog declines are seasonal, and thanks to a lower build rate, the seasonally adjusted backlog-to-build ratio shed a modest 20 basis points to 6.9 months. The current backlog essentially commits the industry into the beginning of 2024.”

Regarding cancellations, McNealy said, “Fleet commitments improved in July but were still somewhat mixed. Total cancels dropped to 1.7% of backlog, following two months of elevated activity.”

McNealy indicates that certain OEMs have informed ACT that customers are reducing their expected orders for the current and upcoming years. Additionally, fewer customers are waiting on the sidelines to take advantage of immediate manufacturing slots as they emerge. Evidently, there is a noticeable change in the demand situation.