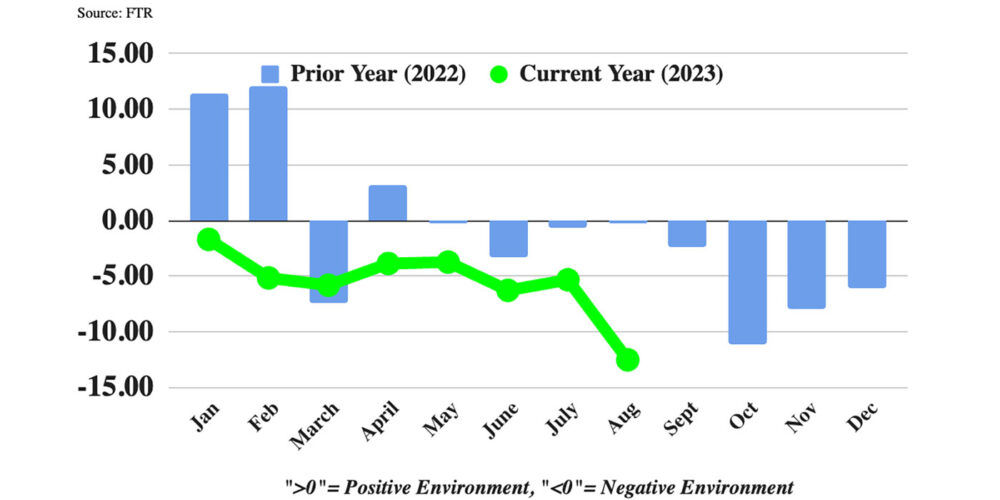

FTR’s Trucking Conditions Index fell to -12.54 in August from the July reading of -5.34 due to sharply higher diesel prices and weaker freight volume. August’s TCI implies the toughest overall market conditions for carriers since April 2020, although surges in fuel prices tend to hurt small operations disproportionately as they are less likely to benefit from fuel surcharges. With fuel costs stabilizing for now, the outlook is for improved conditions, but FTR says that it does not expect the TCI to turn consistently positive until late 2024.

“Market conditions for trucking companies look solidly negative through the first quarter of next year as we forecast no significant strengthening of capacity utilization or freight rates, and freight demand is stagnant,” said Avery Vise, FTR’s vice president of trucking. “A major question is whether consumer spending will remain as strong as it has been in the face of inflation, higher financing costs, and the resumption of debt service of student loan payments.

“Freight demand is more likely to trail our forecast than to exceed it, so any near-term improvements in market conditions for carriers would likely come from a sharp drop in driver capacity. Small carriers continue to exit the market in high numbers, but aside from the LTL sector, larger carriers so far have absorbed much of that capacity. Diesel price volatility and the lack of any near-term strength in spot rates could accelerate carrier failures and tighten capacity.”