During the past six months, trailer manufacturers and major suppliers have largely indicated stable business conditions as compared to each prior month. Responses for May, relative to April, were in line with this trend according to ACT Research. That said, this month’s discussions indicated softer demand for 2024 and mixed concern regarding the supply of labor, according to ACT’s latest State of the Industry report.

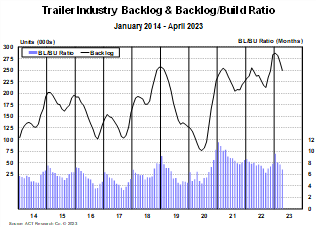

“The seasonally adjusted backlog-to-build ratio dropped 130 basis points month-over-month, to 6.9 months in April, from March’s 8.2-month level,” said Jennifer McNealy, director of CV market research and publications at ACT Research.

Evidencing continued improvements in supply-chain constraints, April’s build per day increased and according to the organization’s research, overall build was 13% lower m/m due to four fewer build days in April than in March. Production growth continues its upswing, and projections point to a continuation of that trend.

“OEMs are reporting that their order boards for 2023 are fully open, with most booked through the end of the year, and we are hearing that some trailer makers are taking orders into 2024,” McNealy said. “That said, several concerns are weighing on their minds, including the labor market, slowing demand into 2024, Fed hikes, business investment providing continued pressure on carrier profitability, recession risk, material supply availability and cost, and how all these factors are likely to impact dealer confidence.”

While the sky isn’t falling, there certainly are some clouds on the horizon that bear watching as we move through the remainder of 2023 and prepare for 2024.