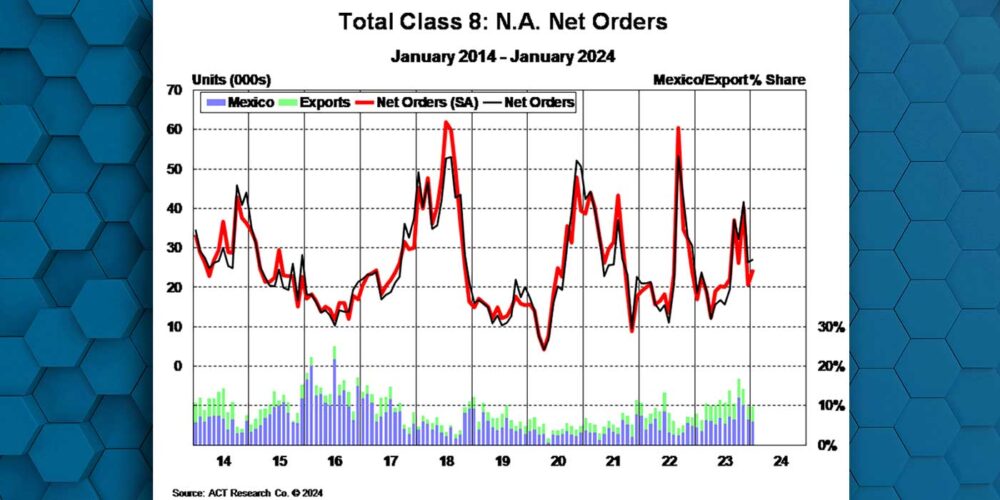

According to the numbers from ACT Research, January Class 8 net orders, at 27,125 units, were up 45% year-over-year. Total Classes 5-7 orders were up 14% y/y at 19,954 units. Kenny Vieth, ACT’s president and senior analyst, called this result surprising.

“Seasonality is one component,” he said, “but given the state of for-hire truckload rates, we continue to suspect private fleets as the primary driver behind U.S. tractor demand. The LTL segment remains a bright spot relative to TL and is likely also contributing. The U.S. economy’s current strength doesn’t hurt either.”

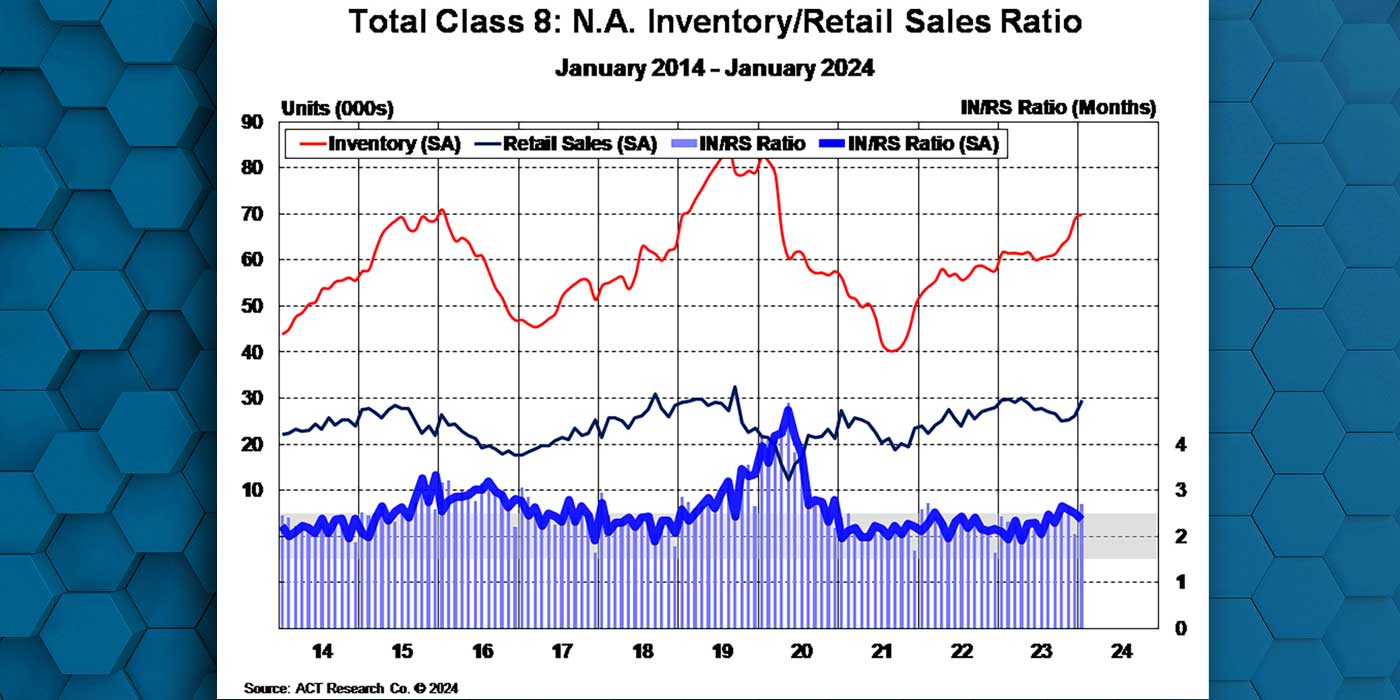

“Class 8 build decreased 7.3% y/y to 26,926 units in January,” Vieth added. “Class 8 inventories rose 1,909 units m/m to 66,277 in January, up 14.3% y/y. Following December’s dash to get equipment finished ahead of regulations starting at the beginning of 2024, Class 8 retail sales totaled 24,500 units in January, up 2.9% y/y. Amid the weakest period of the year for retail sales, and with still strong production, we continue to see risk in the potential for rapid inventory escalation in early 2024.

“Medium-duty build totaled 20,931 units, up 21% y/y. Inventories remain highly elevated, as MD bodybuilder labor challenges persist, totaling 85,330 units nominally, up 31% y/y. Classes 5-7 retail sales remained strong at 19,950 units,” he concluded.