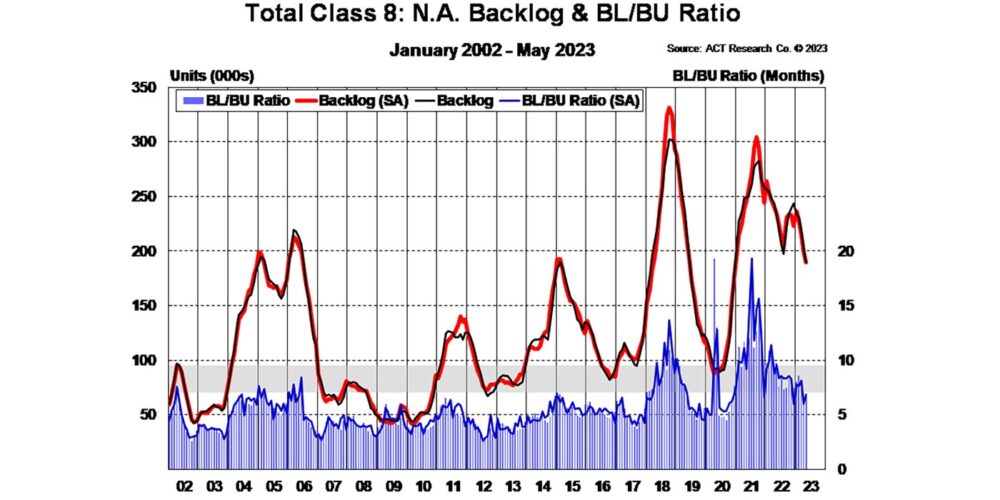

According to ACT Research, the most notable data points this month were heavy duty and medium duty retail sales, each up double digits y/y. Heavy duty cancellations moderated m/m and backlog continues to trend lower, but units scheduled for 2H’23 took a meaningful step higher. Coupling the annual seasonally weak period for orders (typically April-August), with a healthy supply chain enabling and elevating production, the Class 8 backlog should be on a downward trajectory until 2024 orderboards open, according to ACT Research’s latest State of the Industry: North American Classes 5-8 report.

“May’s backlog met expectations, down 13.9k units m/m to 189.2k, and the backlog-to-build ratio decreased 30 basis points m/m to 6.7 months (7.0 seasonally adjusted),” said Eric Crawford, vice president, senior analyst, ACT Research. “Heavy duty and medium duty production were essentially in line with build plans. May’s Class 8 build rate was a healthy 1,343 units per day, representing the ninth month in the past 12 where build rate exceeded 1,300 units per day.”

Regarding sales, he noted, “Heavy duty retail sales remain robust, up 14% y/y at 29,700 units, seasonally adjusted, equivalent to a 357k SAAR. Seasonally adjusted, sales have exceeded 29k units in five of the past six months. Classes 5-7 retail sales were up 26% y/y at 22,800 units.”

Crawford concluded that there will be a decrease in positive progress during the second half of 2023, particularly in the fourth quarter. One significant factor contributing to this is said to be the growing strain on carrier profitability, which is a crucial aspect of heavy vehicle demand. In the first quarter, the profits of public carriers dropped to levels not witnessed since early 2020, according to the recent press release. Although part of this decline was due to seasonal factors, the profit margins of public truckload (TL) carriers decreased by 250 basis points year over year. Considering the projected deterioration of contract rates in the fourth quarter, it is expected that profit margins will continue to narrow.