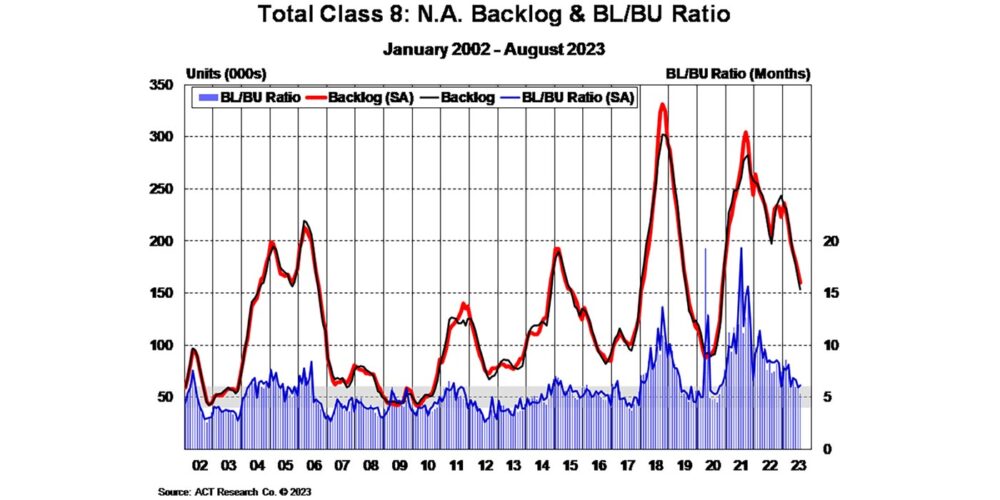

According to the latest numbers from ACT Research, the Class 8 backlog fell by 11,000 units to 152,600 units, based on continued strong build rates and seasonally weak order volumes. At 5.3 months, the nominal backlog-to-build ratio is the lowest it’s been since fall 2020, ACT’s reporting found.

“The Class 8 backlog is likely to turn higher in the near term as 2024 order season begins. The Classes 5-7 backlog fell 3,100 units to 113,900 units in August,” said Kenny Vieth, president and senior analyst at ACT Research. “The backlog-to-build ratio rose to 5.3 months from 4.7 in July on a lower daily build rate.”

August is one of the weakest months of the year for Class 8 orders, as out-year orderboards are not typically fully open, ACT says. While the tractor market appears under pressure heading into 2024 amid weak freight and falling carrier profits, vocational truck demand remains strong. August saw net orders up 3,900 units month-over-month to 19,500 units, with vocational trucks accounting for 42% of orders in August, well above the historical average around 29%.

Vieth’s conclusion is that despite a strong economy boosting demand, the freight markets are still stuck in a low point in their cycle. This is because private fleets are increasing their capacity and taking on more freight, which is limiting the demand for for-hire services. While there is currently a backlog of demand for equipment, particularly tractors, this is expected to decrease by the end of the year. However, it’s worth noting that the plans for building new equipment haven’t yet reflected the significant drops in freight rates and carrier profits, he added.